0:12 AM Low Home Loan Rates - What You Need to Know Before It - s Too Late | ||||

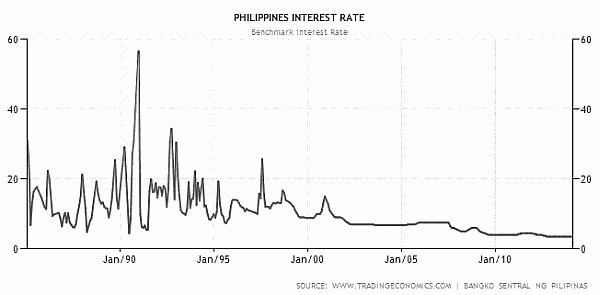

#housing loan interest rates # Low Home Loan Rates What You Need to Know Before It s Too LateUpdated on May 5, 2015 by Jay Castillo 51 Comments ADVERTISEMENT Have you seen the low interest home loans being offered by a few banks out there lately? in 2011, the lowest home loan rate I have seen was 5.99% per year. As I update this, it is now even lower at 5.25%. Personally, I believe these are the best home loan rates I have ever seen in my lifetime. This even beats the 6.0% interest rate offered by the GSIS before . This sounds tempting. not just for real estate investors. but also for home buyers . But wait, before you apply for a home loan. you need to know that the low interest rate is fixed only for the first year and can be quite risky Lower home loan rates meanBefore I discuss the risks, let me first focus on the positive. Obviously, the biggest impact of having a low interest rate on your home loan would be a significant drop in the monthly amortization payments. Let s say you are going to buy a foreclosed property and the loan amount is Php2,000,000. If we use the usual 12% as the annual interest rate, at 10 years to pay, that would mean a monthly amortization of Php28, 694.19 . (I used our very own mortgage calculator which can be found here: Home Loan / Mortgage Calculator ). In contrast, if we used an interest rate of 5.25%. using the same loan parameters above, the resulting monthly amortization would be just Php21,458.43. This means a discount of Php7,235.76 per month in monthly amortization payments. The savings in monthly payments is quite significant right? Imagine if you had several rental properties. This could translate to more positive cashflow. In addition, I checked one of the banks that offer these low interest rates, and found out that the same rate is also applicable if one wants to refinance a home loan. I was surprised because I was expecting different home loan refinance rates . This could be useful for real estate investors who want to get some cash out of their equity through refinancing, provided they are in good standing. I guess getting a new home loan for people with bad credit is out of the question. Here s the fine printAs with most things, there s a fine print. In this case, the low interest rate is only fixed for the first year, and is subject to yearly repricing thereafter. This means that after the first year, one is at the mercy of interest rate fluctuations. What if there was another financial crisis (knock on wood ), and interest rates suddenly went up. If that happens, there would be an increase in the interest rate to be used come repricing time, and would result in a corresponding increase in the monthly amortization payments. By the way, some banks also offer some form of rate protection where the increase of the interest rate is limited to 2%. This is similar to the practice of Pag-IBIG. However, if one chose the option to have the interest rate fixed for only a year, it s possible that the interest rate will be increased yearly right? ScenariosIf you are a real estate investor and have rental properties purchased through home loans, the increase in monthly amortization payments can turn a nice positive cashflow generating property into one that is negatively geared, which is like a money pit. It can swallow up all of your money. To illustrate, if interest rates jumped to 20%, the monthly payment for the example above would become a staggering Php38,651.13 per month. This is really possible and has actually happened during the Asian financial crisis in 1997 when the interest rates exceeded 20%. It is well-settled that history repeats itself, and real estate is cyclical, so it is possible that this will happen again.

Raising rents to cover the additional monthly payments can only work up to a certain extent and may not be enough, especially if a property is covered by the rent control law. Besides, market forces dictate rental rates and increasing it might drive tenants away, making the situation worse. ADVERTISEMENT The same applies to non-investors. Unless one s source of income, which is usually just one s salary, more than covers any sudden increase in the monthly amortization payments, he is in danger of defaulting on his mortgage loan payments. A salary increase would help, but usually the opposite happens during bad times as businesses also try to save on expenses. This can even lead to foreclosure down the road. In such harsh economic conditions during a financial crisis, the usual steps one can take to avoid foreclosure may offer little help and not work at all. Nevertheless, I believe that the scenarios described above can be easily avoided by simply going for fixed interest rates . Why go for fixed interest rates?I believe that the proactive thing to do would be to go for fixed interest rates for the longest term possible. This eliminates the risk of being subject to sudden interest rate fluctuations, all throughout the loan term. Sure, the interest rates usually become higher, the longer they are fixed, but at least, you are protected just in case prevailing interest rates shoot up due to economic conditions. Anyway, If you are really concerned about the higher fixed interest rates for longer terms, my suggestion would be to have something in the middle, let s say 5 years for example, provided you are prepared to have the loan fully paid before the end of the 5th year, if needed. This seems to be a more balanced approach as you still get protection, but the interest rate at the start should not be too high. What the heck, if you believe you can pay in full for a property in one year, then by all means, go for the lowest home loan rate you can find, even if it is just fixed for a year. My point is simple, I suggest going for a fixed interest rate, with the longest term possible, so that at the very least, you will have enough time to pay-off the home loan to avoid any repricing, if interest rates really do go up. This will help minimize your risks, and have peace of mind, which I believe is priceless. Happy investing! To our success and financial freedom! Jay Castillo Real Estate Investor Real Estate Broker License #: 3194

| ||||

|

| ||||

| Total comments: 0 | |